Introduction:

grplasso is a specialized R package designed for fitting

penalized regression models in settings involving high-dimensional

grouped (or clustered) effects. Unlike traditional lasso approaches that

treat all covariates equally, grplasso distinguishes and efficiently

handles group structures to improve the computational performance.

This tutorial demonstrates how to apply grplasso in

practice using illustrative example datasets.

Installation:

require("devtools")

require("remotes")

remotes::install_github("UM-KevinHe/grplasso", ref = "main")Quick Start:

In this section, we will explore the fundamental usage of the functions integrated into the current R package, providing a detailed interpretation of the resulting values obtained from these functions. To enhance users’ understanding of the R package, we will employ example datasets, enabling a comprehensive grasp of its functionalities.

library(grplasso)

#> Error in get(paste0(generic, ".", class), envir = get_method_env()) :

#> object 'type_sum.accel' not found1. Generalized Linear Models (GLMs)

To exemplify the process of fitting a generalized linear model, we will utilize the “BinaryData” dataset included in the package. This dataset consists of five predictors, an indicator for provider information, and a binary outcome variable.

data(BinaryData)

data <- BinaryData$data

Y.char <- BinaryData$Y.char # variable name of outcome variable

prov.char <- BinaryData$prov.char # variable name of provider indicator

Z.char <- BinaryData$Z.char # variable names of predictors

head(data)

#> Y Prov.ID Z1 Z2 Z3 Z4 Z5

#> 1 1 10 -0.006 -0.159 0.588 0.378 -1.430

#> 2 0 11 0.862 -0.162 0.243 0.503 0.549

#> 3 0 11 0.453 0.961 0.665 0.522 0.859

#> 4 1 8 -0.286 0.001 0.903 0.886 -0.324

#> 5 0 13 0.564 -0.194 -0.062 -0.792 -0.783

#> 6 1 18 0.676 1.095 2.223 1.367 1.060Without grouped covariate

The pp.lasso() function is employed to fit a generalized

linear model when the covariate does not include any group information.

When the user does not specify the regularization coefficient

,

our function automatically generates a sequence of

values by default. The sequence starts with the largest

,

which penalizes all covariates to zero, and then gradually decreases

to allow for variable selection and modeling flexibility.

fit <- pp.lasso(data, Y.char, Z.char, prov.char)The coef() function serves to provide estimates of the

coefficients in the fitted model. The resulting coefficient matrix is

structured such that the column names correspond to the

values used in the modeling process.

coef(fit)$beta[, 1:5]

#> 0.132 0.1202 0.1096 0.0998 0.091

#> Z1 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z2 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z3 0 0.1120347 0.2148847 0.3098777 0.3980465

#> Z4 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z5 0 0.0000000 0.0000000 0.0000000 0.0000000

coef(fit)$gamma[1:5, 1:5]

#> 0.132 0.1202 0.1096 0.0998 0.091

#> 1 -0.2411977 -0.2939898 -0.3431091 -0.3889330 -0.4318211

#> 2 -1.9635362 -1.8742433 -1.7984115 -1.7336457 -1.6779754

#> 3 -1.2089403 -1.1883078 -1.1712888 -1.1572109 -1.1455229

#> 4 -1.9600386 -1.8922127 -1.8332183 -1.7815619 -1.7360041

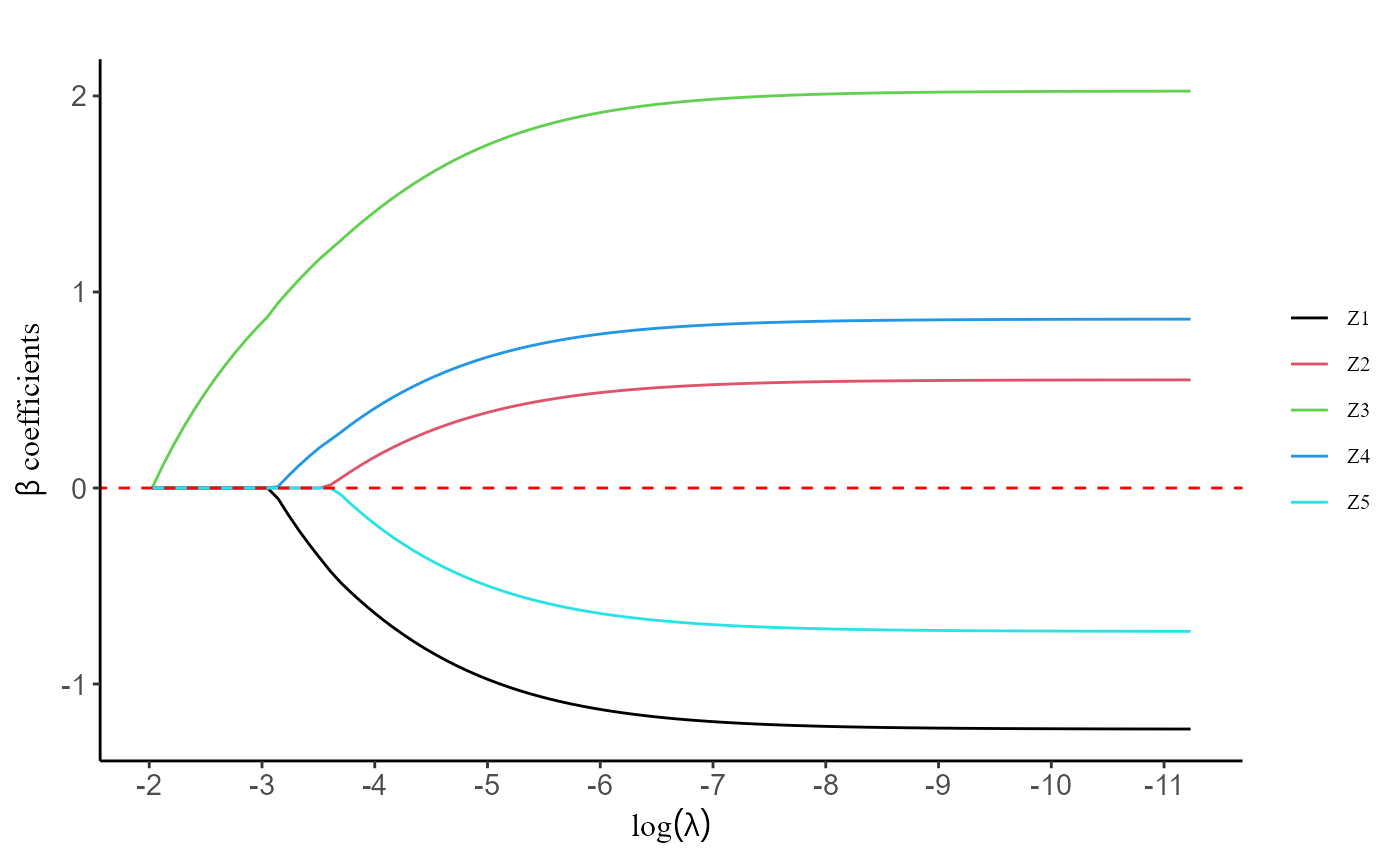

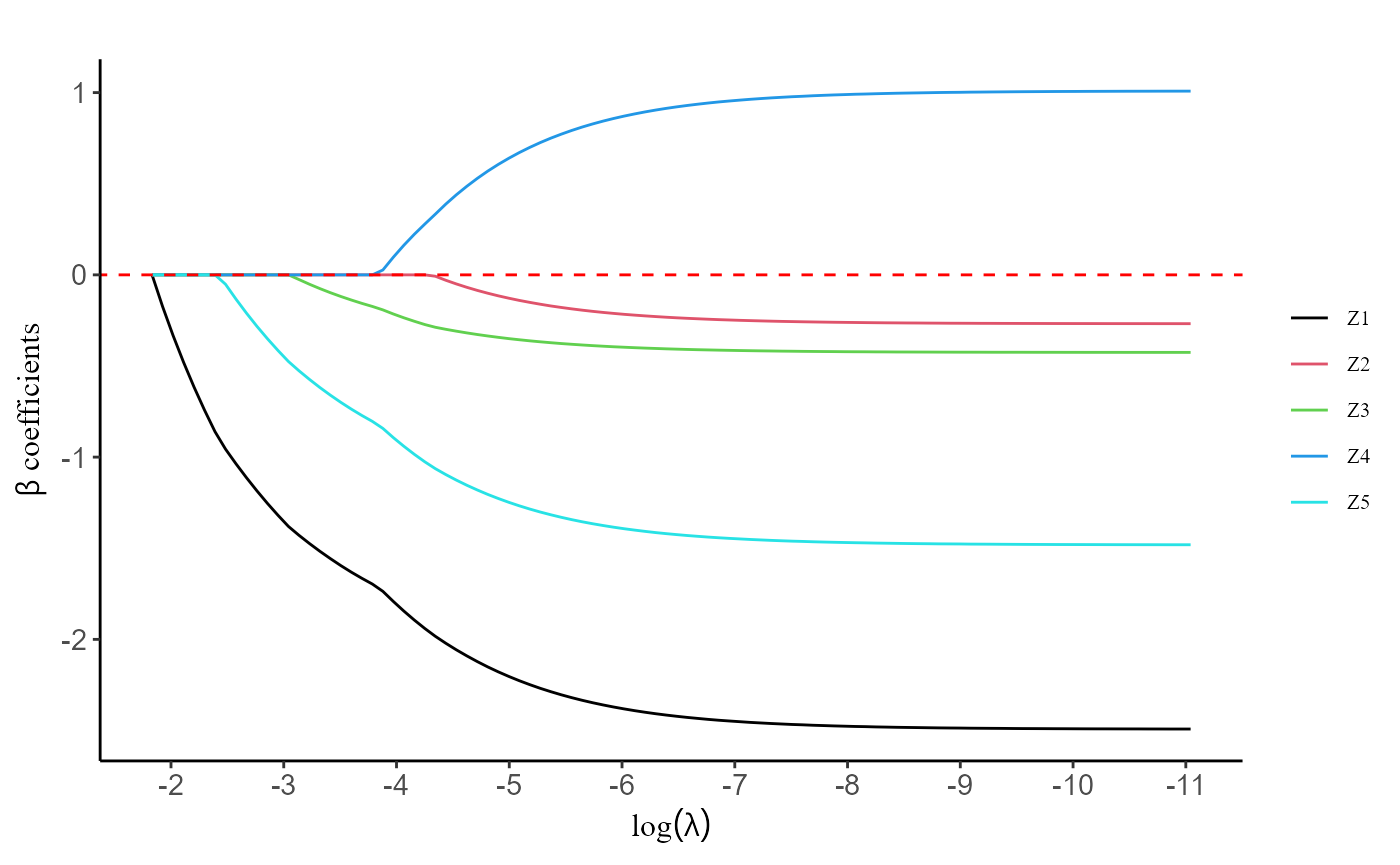

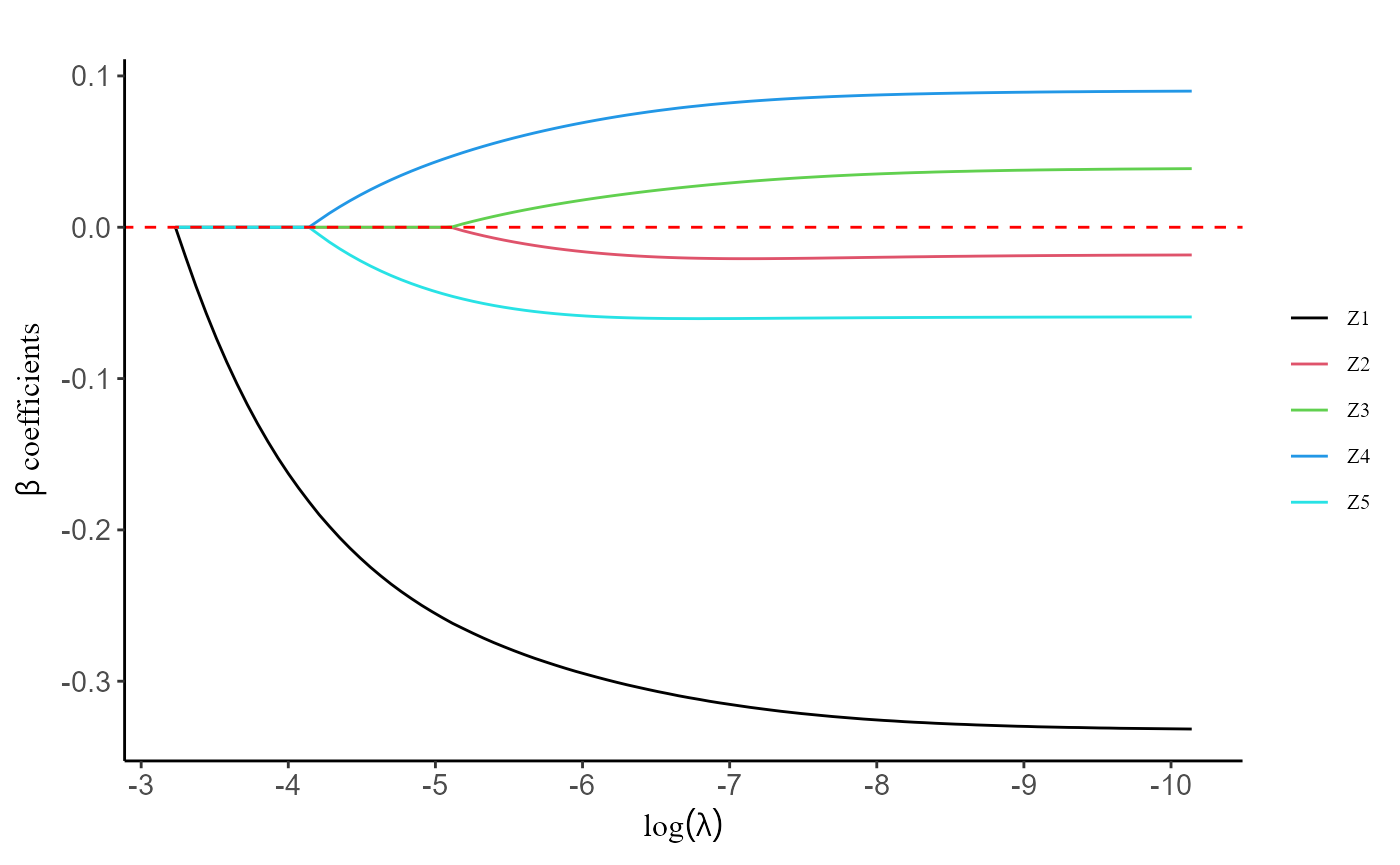

#> 5 -0.5500569 -0.5698456 -0.5894538 -0.6087582 -0.6276779The plot() function is designed to generate a figure

depicting the regularization path. This path illustrates the behavior of

the coefficients for each predictor variable as the regularization

parameter

varies. By visualizing the regularization path, users can gain valuable

insights into the impact of different regularization strengths on the

coefficients, aiding in model interpretation and selection.

plot(fit, label = TRUE)

The predict() function is utilized to generate model

predictions for a given dataset based on the coefficient estimates

obtained from the fitted model. Once the model has been trained using

the pp.lasso() function and the coefficients have been

estimated, the predict function can be applied to new data to obtain

predictions for the outcome variable.

This function offers various types of outputs to suit different analysis needs. For instance, when fitting a penalized logistic regression model, using type = “response” provides the probabilities of “Y = 1” for each observation, while type = “class” provides the predicted class.

predict(fit, data, Z.char, prov.char, lambda = fit$lambda, type = "response")[1:5, 1:5]

#> 0.132 0.1202 0.1096 0.0998 0.091

#> [1,] 0.2874999 0.2996927 0.3106971 0.3206762 0.3297643

#> [2,] 0.2051302 0.2112109 0.2163924 0.2208163 0.2246015

#> [3,] 0.2051302 0.2191951 0.2321638 0.2441339 0.2551989

#> [4,] 0.3947391 0.4208778 0.4449423 0.4671087 0.4875485

#> [5,] 0.2345694 0.2340619 0.2330311 0.2316163 0.2299295

predict(fit, data, Z.char, prov.char, lambda = 0.001, type = "class")[1:5]

#> [1] 1 0 0 1 0With grouped covariate

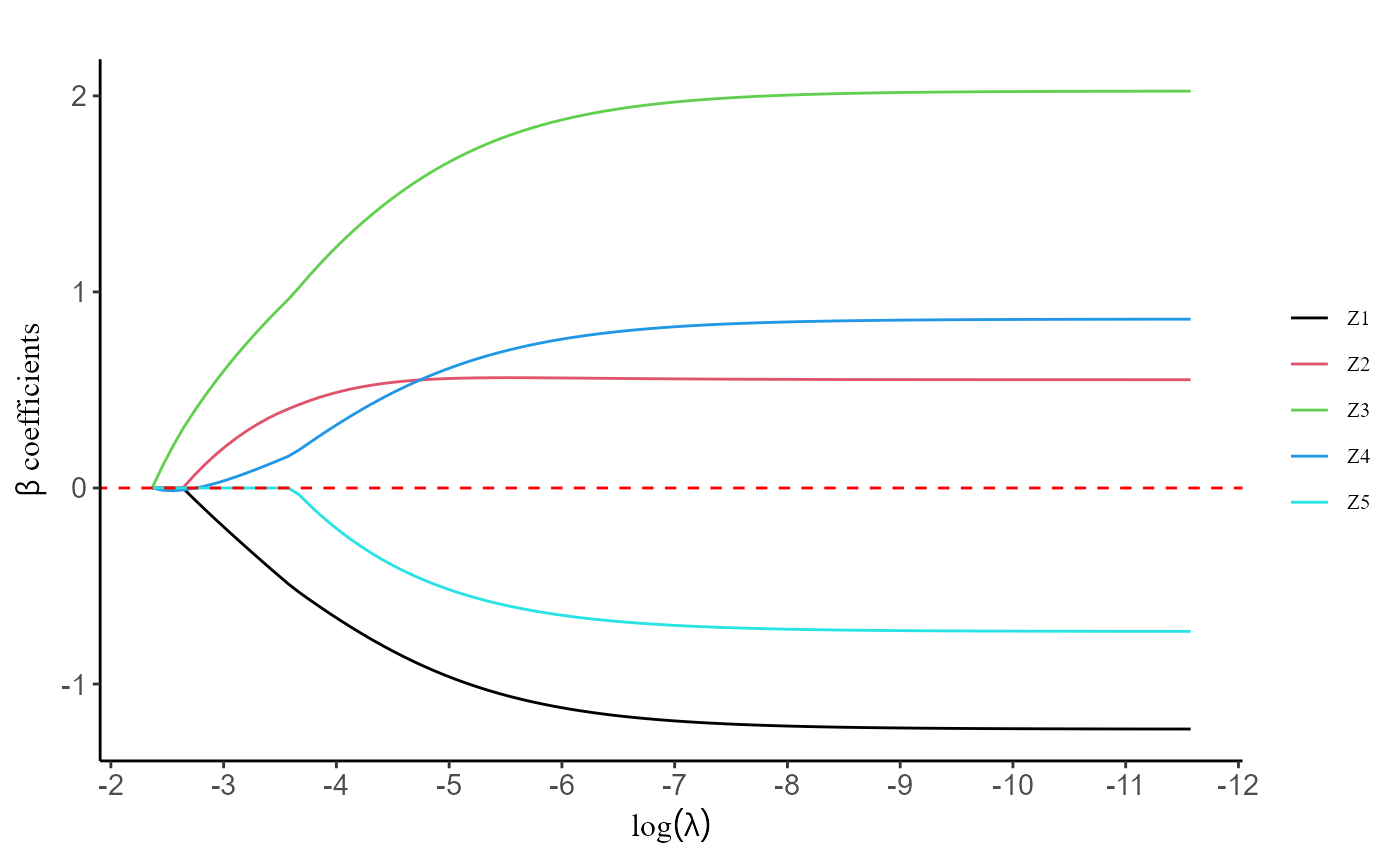

The utilization of the grp.lasso() function is similar

to the previously mentioned methods, with the added requirement of

providing group information for the covariates. When calling the

function, users should provide the necessary group information to ensure

proper grouping of variables for regularization. However, if the user

does not explicitly provide the group information, the

grp.lasso() function will automatically assume that each

variable is treated as an individual group on its own. This default

behavior simplifies the process for users who do not wish to specify

explicit groups, ensuring that the function can still be applied

effectively without the need for additional input.

group <- BinaryData$group

fit2 <- grp.lasso(data, Y.char, Z.char, prov.char, group = group)

plot(fit2, label = T)

Please note that for both pp.lasso() and

grp.lasso() functions, the parameter “prov.char” is

optional. In the event that the user does not specify the provider

information for the observations, the program will automatically assume

that all observations originate from the same health provider, resulting

in the generation of one common intercept.

fit.no_prov <- pp.lasso(data, Y.char, Z.char)

#> Warning: Provider information not provided. All data is assumed to originate

#> from a single provider!

coef(fit.no_prov)$beta[, 1:5]

#> 0.2513 0.2289 0.2086 0.1901 0.1732

#> Z1 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z2 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z3 0 0.1006904 0.1935559 0.2800125 0.3610722

#> Z4 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z5 0 0.0000000 0.0000000 0.0000000 0.0000000

coef(fit.no_prov)$gamma[1:5] #"gamma" is treated as the common intercept

#> 0.2513 0.2289 0.2086 0.1901 0.1732

#> -0.5838804 -0.5896897 -0.5974013 -0.6065479 -0.6167685Regularization parameter selection for GLM problems

The optimal regularization parameter

()

is determined through cross-validation. To find the best

,

users can employ either the cv.pp.lasso() or

cv.grp.lasso() function, depending on the specific type of

model they are working with. These cross-validation functions inherit

the parameters required for the model fitting process, providing a

seamless and straightforward experience for users. By default, both

functions utilize 10-fold cross-validation.

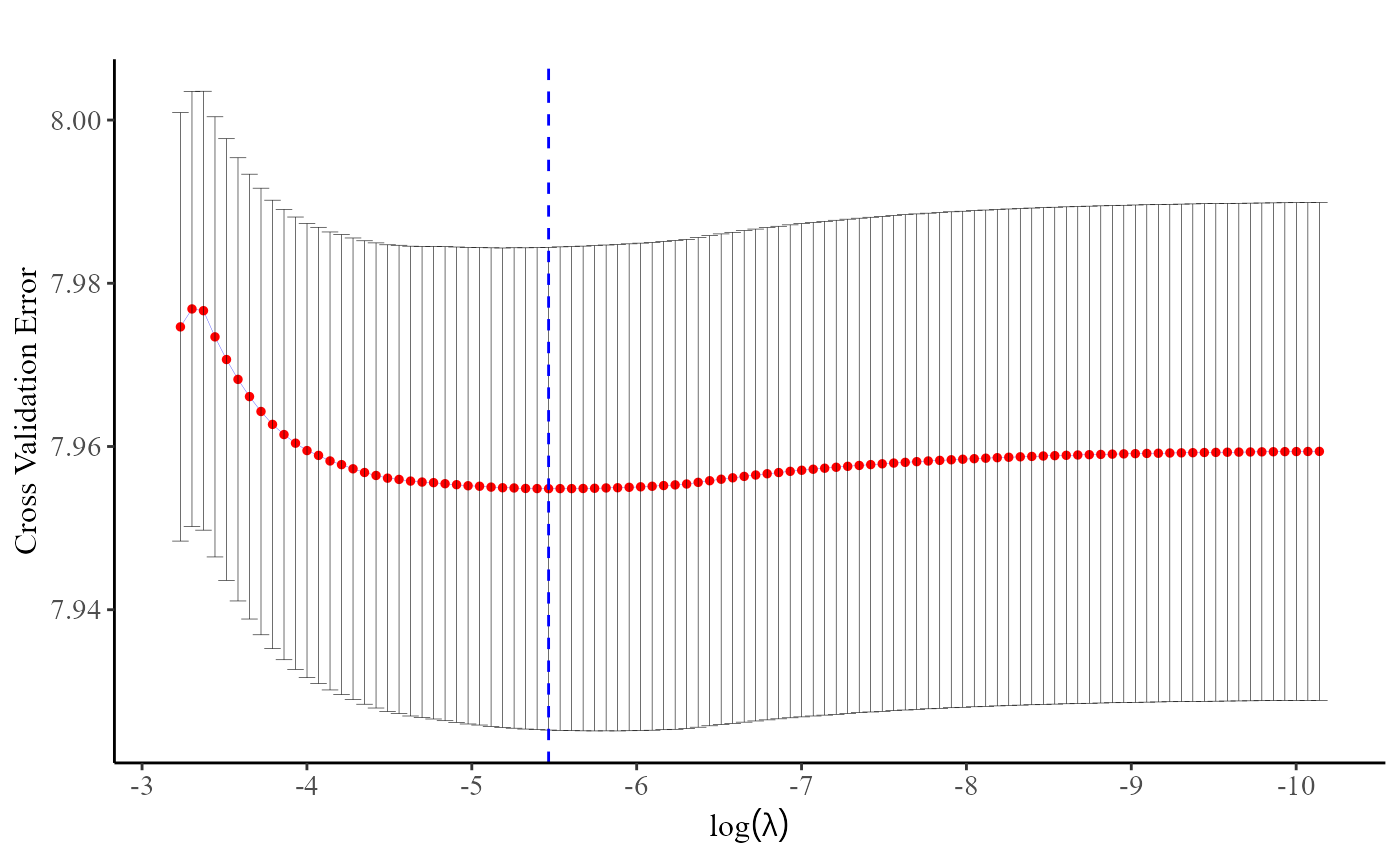

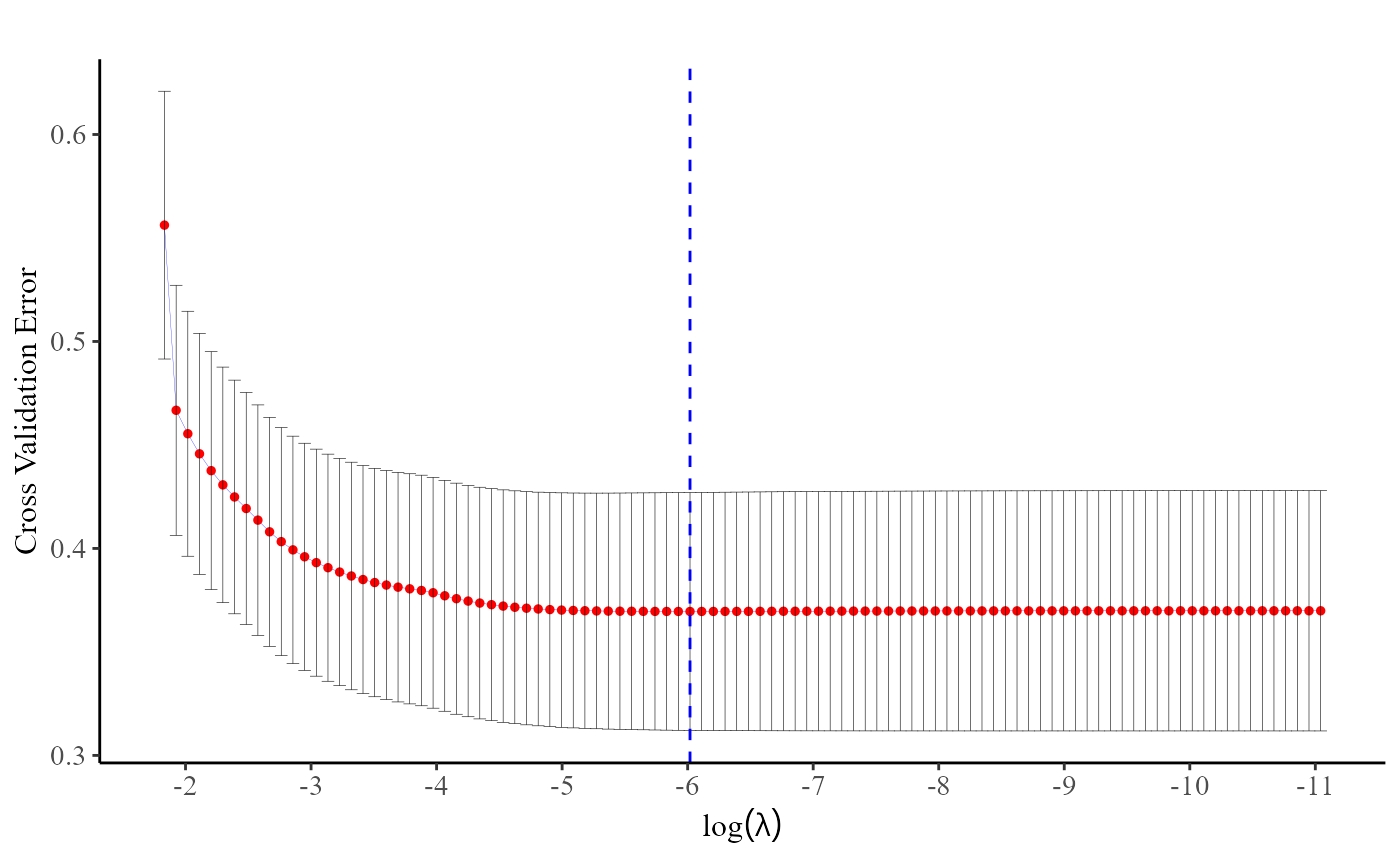

fit <- cv.pp.lasso(data, Y.char, Z.char, prov.char, nfolds = 10)The plot() function, applied to a

cv.pp.lasso or cv.grp.lasso object, generates

a figure that enables users to assess how the cross-entropy loss changes

with varying values of

.

By observing the plot, users can easily identify the point at which the

cross-entropy loss is minimized.

plot(fit)

Indeed, users can directly use the fit$lambda.min command to obtain the optimal value of .

fit$lambda.min

#> [1] 0.0012595912. Discrete Survival Models

The pp.DiscSurv() function is utilized for fitting a

penalized discrete survival model. In contrast to the current R package,

this function does not necessitate data expansion based on discrete time

points, resulting in a significant reduction in memory usage and

convergence time required for operation.

The DiscTime dataset, included in this package,

comprises of 5 covariates, provider information, observation time, and

event indicator. We will be using this dataset as an example to

illustrate how to utilize it.

data(DiscTime)

data <- DiscTime$data

Event.char <- DiscTime$Event.char

Time.char <- DiscTime$Time.char

head(data)

#> Prov.ID Z1 Z2 Z3 Z4 Z5 time status

#> 1 4 -1.298 -1.471 -1.346 -1.775 -1.241 1.03 1

#> 2 5 0.192 0.163 0.953 1.083 0.371 12.50 0

#> 3 4 -2.315 -2.038 -1.629 -2.577 -2.008 0.53 1

#> 4 1 -0.198 1.231 0.633 0.739 0.214 6.74 1

#> 5 2 0.469 0.640 -0.583 0.161 0.927 12.50 0

#> 6 4 -1.445 -1.848 -3.024 -2.117 -1.894 0.53 1

fit <- pp.DiscSurv(data, Event.char, prov.char, Z.char, Time.char)The pp.DiscSurv() function yields three main sets of

coefficients as its primary output. These coefficients pertain to the

covariate estimates, log-transformed baseline hazard for various time

points, and provider effects. To avoid multicollinearity problems, we

designate the first provider as the reference group.

Similar to the GLM fitting functions mentioned earlier,

pp.DiscSurv() is also furnished with a coef()

function. This function facilitates the provision of coefficient

estimates within the fitted penalized discrete survival model across the

entire sequence of

values employed in the modeling procedure.

coef(fit)$beta[, 1:5]

#> 0.1601 0.1458 0.1329 0.1211 0.1103

#> Z1 0 -0.1735757 -0.3325774 -0.4793679 -0.6155647

#> Z2 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z3 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z4 0 0.0000000 0.0000000 0.0000000 0.0000000

#> Z5 0 0.0000000 0.0000000 0.0000000 0.0000000

coef(fit)$gamma[, 1:5]

#> 0.1601 0.1458 0.1329 0.1211 0.1103

#> 1 0.0000000 0.0000000 0.000000 0.0000000 0.0000000

#> 2 -4.5665147 -4.3516946 -4.162992 -3.9945779 -3.8425705

#> 3 -0.7478311 -0.7116142 -0.682481 -0.6580980 -0.6367834

#> 4 1.2412090 1.1456446 1.059286 0.9815198 0.9121089

#> 5 -2.3399410 -2.1966372 -2.070536 -1.9577270 -1.8555876

coef(fit)$alpha[, 1:5]

#> 0.1601 0.1458 0.1329 0.1211 0.1103

#> [Time: 0.53] -1.668065 -1.747753 -1.824209 -1.898663 -1.971909

#> [Time: 1.03] -1.480994 -1.526815 -1.571328 -1.615488 -1.659886

#> [Time: 3.92] -1.622145 -1.641556 -1.661848 -1.683563 -1.706991

#> [Time: 6.74] -1.251585 -1.257340 -1.264124 -1.272503 -1.282795

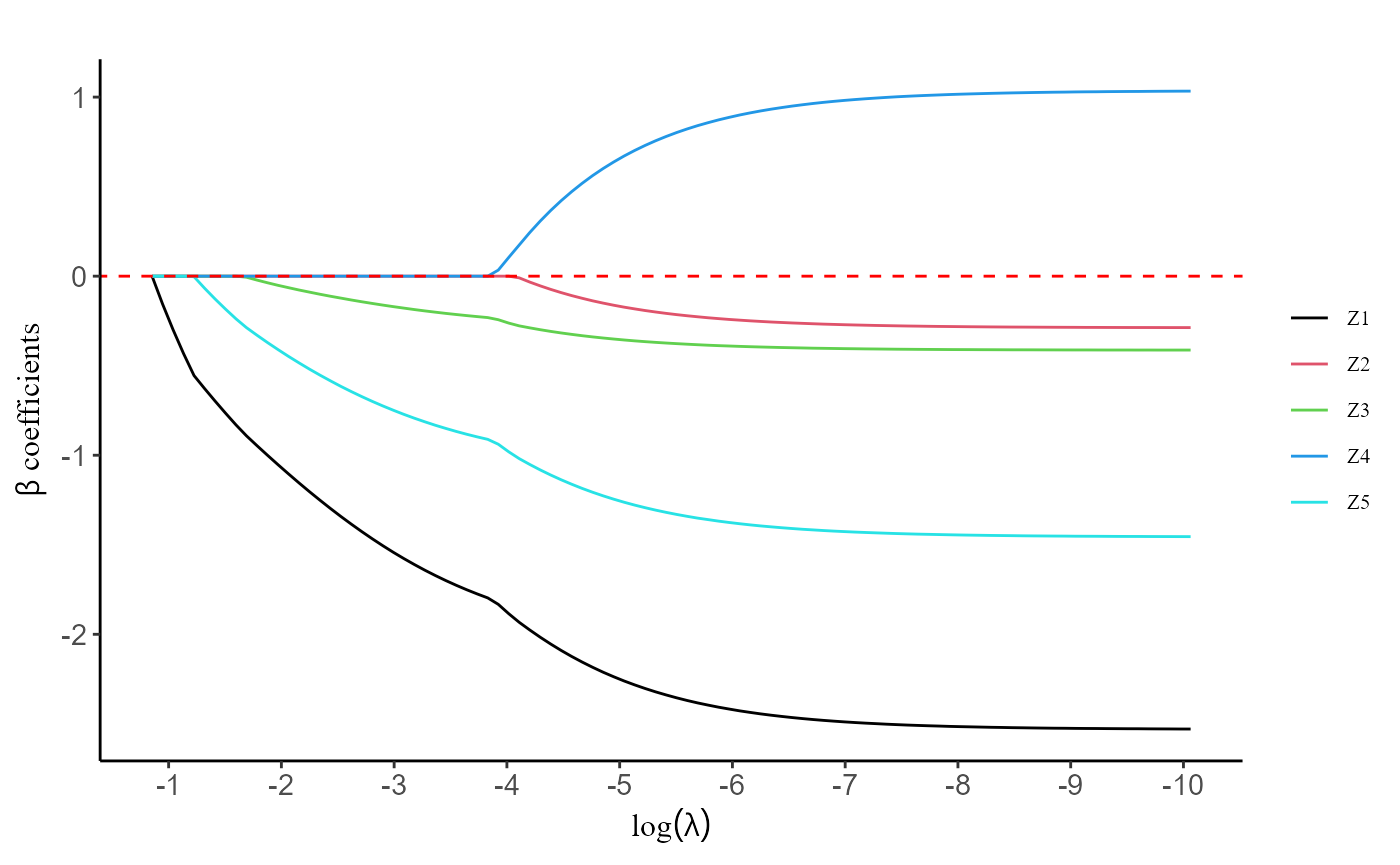

#> [Time: 12.5] -1.781635 -1.780095 -1.780526 -1.783340 -1.788771Users have the option to utilize the plot() function,

which generates a figure illustrating the regularization path. This

visual representation showcases the behavior of the coefficients for

each predictor variable as

varies.

plot(fit, label = T)

The predict() function is employed to generate model

predictions for a given dataset using the coefficient estimates obtained

from the fitted model. It is essential to note that the discrete time

points within the prediction data set must align with the discrete time

points used during model fitting. If they do not match, the baseline

hazard of mismatches cannot be estimated accurately.

predict(fit, data, Event.char, prov.char, Z.char, Time.char, lambda = fit$lambda, type = "response", which.lambda = fit$lambda[1])[1:5,]

#> Individual [Time: 0.53] [Time: 1.03] [Time: 3.92] [Time: 6.74] [Time: 12.5]

#> 1 1 0.1586823 0.1852773 NA NA NA

#> 2 2 0.1586823 0.1852773 0.1649092 0.2224258 0.1441013

#> 3 3 0.1586823 NA NA NA NA

#> 4 4 0.1586823 0.1852773 0.1649092 0.2224258 NA

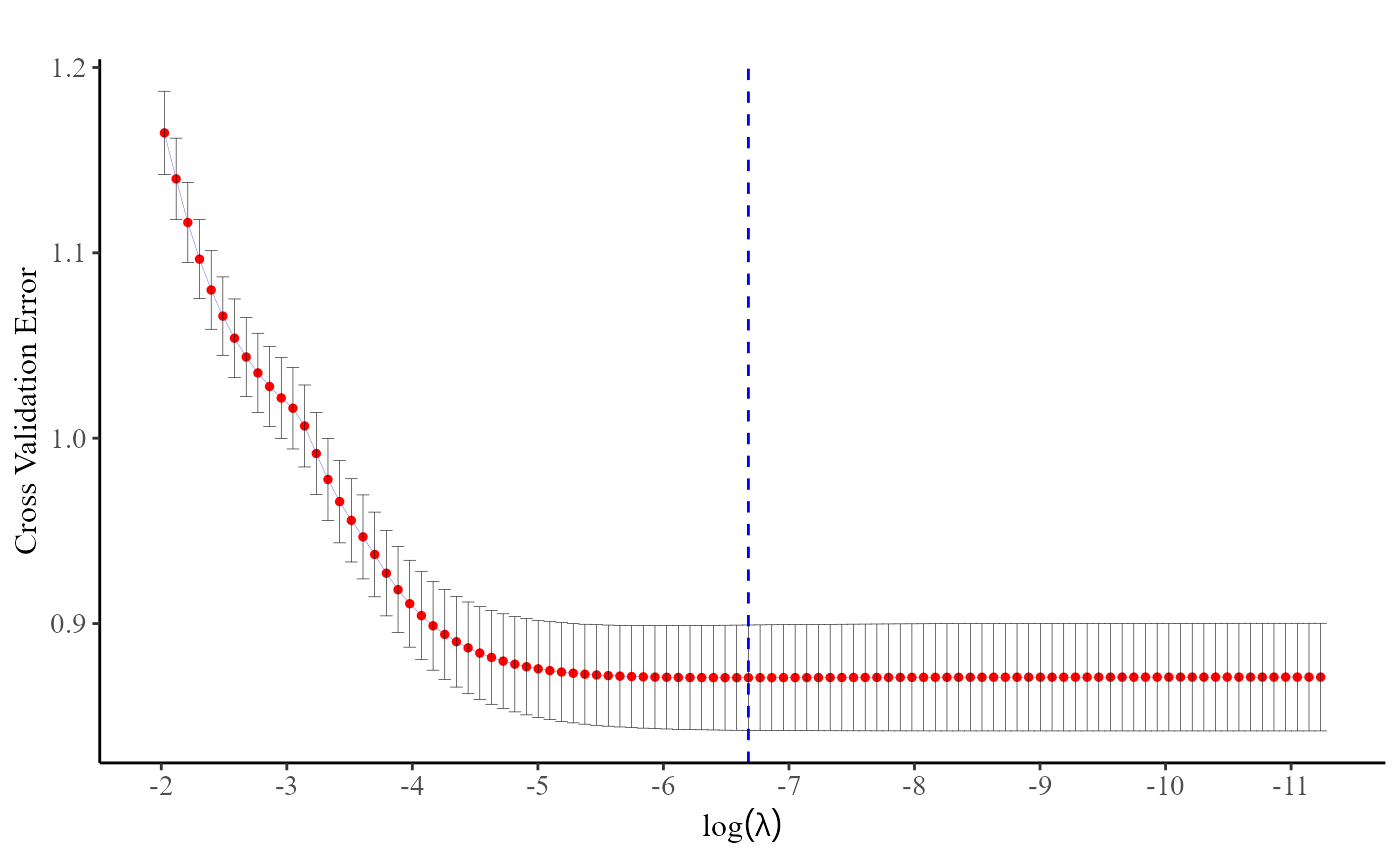

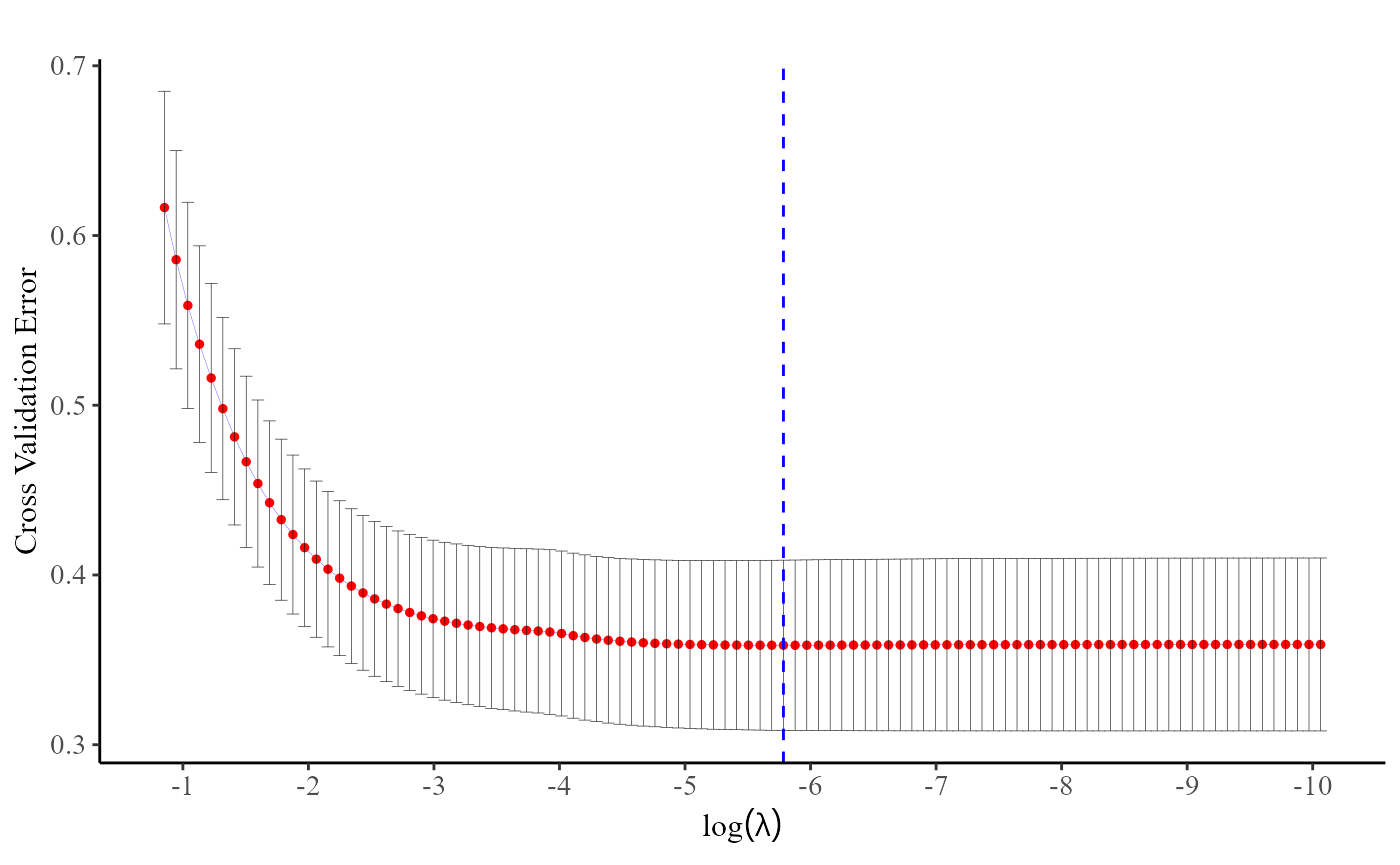

#> 5 5 0.1586823 0.1852773 0.1649092 0.2224258 0.1441013Regularization parameter selection for discrete survival models

The optimal regularization parameter

()

is determined through cross-validation, utilizing the cross-validation

error as the guiding metric. Users can identify the best

value by employing the cv.pp.DiscSurv() function.

fit <- cv.pp.DiscSurv(data, Event.char, prov.char, Z.char, Time.char, nfolds = 10, trace.cv = T)

#> Starting CV fold #1...

#> Starting CV fold #2...

#> Starting CV fold #3...

#> Starting CV fold #4...

#> Starting CV fold #5...

#> Starting CV fold #6...

#> Starting CV fold #7...

#> Starting CV fold #8...

#> Starting CV fold #9...

#> Starting CV fold #10...Users can either utilize the plot() function or directly

access the fit$lambda.min command to identify the optimal value

of

at which the cross-entropy loss is minimized.

plot(fit)

fit$lambda.min

#> [1] 0.00243264Discrete survival model with no grouped (or clusted) information provided

Similar with our GLM-related functions, we present a solution for fitting a discrete survival model without requiring provider information. This approach tackles the issue commonly encountered with existing statistical tools used to fit discrete survival models, which often necessitate data expansion, leading to significantly slow convergence.

For ease of use, we have introduced a new function called

DiscSurv(), designed to facilitate a similar user

experience to pp.DiscSurv(). However, the key difference

lies in the fact that DiscSurv() no longer demands provider

information from the user, meaning that all observations are now treated

as originating from the same healthcare provider.

Additionally, we have provided the cv.DiscSurv()

function to aid users in selecting optimal

.

Moreover, the coef(), predict(), and

plot() functions have also been thoughtfully

incorporated.

fit <- DiscSurv(data, Event.char, Z.char, Time.char) # no provider information required

coef(fit, lambda = fit$lambda)$alpha[, 1:10] #time effect

#> 0.4261 0.3882 0.3537 0.3223 0.2937 0.2676

#> [Time: 0.53] -1.979501 -1.970055 -1.977003 -1.996580 -2.025956 -2.063289

#> [Time: 1.03] -2.110213 -2.069229 -2.043936 -2.030857 -2.027098 -2.024884

#> [Time: 3.92] -2.484907 -2.418504 -2.367851 -2.329504 -2.300539 -2.271883

#> [Time: 6.74] -2.355695 -2.272311 -2.204520 -2.148985 -2.102832 -2.057118

#> [Time: 12.5] -2.958691 -2.863140 -2.784495 -2.719193 -2.664086 -2.607955

#> 0.2438 0.2221 0.2024 0.1844

#> [Time: 0.53] -2.108335 -2.159552 -2.215497 -2.275267

#> [Time: 1.03] -2.029997 -2.041139 -2.057146 -2.077164

#> [Time: 3.92] -2.250817 -2.236107 -2.226728 -2.221906

#> [Time: 6.74] -2.019042 -1.987381 -1.961174 -1.939721

#> [Time: 12.5] -2.560084 -2.519189 -2.484282 -2.454649

coef(fit, lambda = fit$lambda)$beta[, 1:10] #covariate coefficient

#> 0.4261 0.3882 0.3537 0.3223 0.2937 0.2676 0.2438

#> Z1 0 -0.1556065 -0.2988513 -0.4321738 -0.555131105 -0.62728969 -0.6971121

#> Z2 0 0.0000000 0.0000000 0.0000000 0.000000000 0.00000000 0.0000000

#> Z3 0 0.0000000 0.0000000 0.0000000 0.000000000 0.00000000 0.0000000

#> Z4 0 0.0000000 0.0000000 0.0000000 0.000000000 0.00000000 0.0000000

#> Z5 0 0.0000000 0.0000000 0.0000000 -0.003068977 -0.06697318 -0.1271421

#> 0.2221 0.2024 0.1844

#> Z1 -0.7648862 -0.8306053 -0.891723581

#> Z2 0.0000000 0.0000000 0.000000000

#> Z3 0.0000000 0.0000000 -0.005878473

#> Z4 0.0000000 0.0000000 0.000000000

#> Z5 -0.1840291 -0.2383354 -0.287531205

plot(fit, label = T)

cv.fit <- cv.DiscSurv(data, Event.char, Z.char, Time.char, nfolds = 10, trace.cv = T)

#> Starting CV fold #1...

#> Starting CV fold #2...

#> Starting CV fold #3...

#> Starting CV fold #4...

#> Starting CV fold #5...

#> Starting CV fold #6...

#> Starting CV fold #7...

#> Starting CV fold #8...

#> Starting CV fold #9...

#> Starting CV fold #10...

plot(cv.fit)

predict(fit, data, Event.char, Z.char, Time.char, lambda = fit$lambda, type = "response", which.lambda = cv.fit$lambda.min)[1:5,]

#> Individual [Time: 0.53] [Time: 1.03] [Time: 3.92] [Time: 6.74] [Time: 12.5]

#> 1 1 0.491864462 0.74764296 NA NA NA

#> 2 2 0.009860994 0.02957994 0.041247655 0.07816691 0.05422556

#> 3 3 0.952556420 NA NA NA NA

#> 4 4 0.020209741 0.05938188 0.081813820 0.14938494 NA

#> 5 5 0.001765611 0.00538432 0.007582723 0.01483601 0.010079863. Stratified Cox Models

Our R package offers the Strat.cox() and

cv.strat_cox() functions designed for fitting penalized

stratified Cox models. In the context of our intended scenario, each

healthcare provider is considered a distinct stratum. The functionality

of both Strat.cox() and cv.strat_cox() extends

to the incorporation of group information among variables, achieved by

configuring the “group” parameter.

We employ the ContTime simulation dataset, which is

included within this package, to illustrate the utilization of these two

functions. This dataset encompasses five covariates, a provider

indicator (which serves as stratum information), as well as follow-up

time and event indicators.

data(ContTime)

data <- ContTime$data

head(data)

#> Prov.ID Z1 Z2 Z3 Z4 Z5 status time

#> [1,] 11 3.431888 4.397010 3.800101 4.809899 4.049038 1 0.4984520

#> [2,] 4 2.789097 2.616714 3.401736 3.510431 3.650074 0 3.0000000

#> [3,] 9 5.451523 4.009896 5.473275 4.772835 4.708293 1 0.5987062

#> [4,] 15 2.421634 2.284766 1.747758 2.182607 1.072065 1 0.6406964

#> [5,] 9 5.827436 5.238138 5.536604 5.265083 4.735679 0 3.0000000

#> [6,] 18 2.140707 1.773304 1.792366 1.774502 3.209669 0 3.0000000Users can utilize the coef() function to obtain

coefficient estimates for the covariates across the complete sequence of

values.

coef(fit)[, 1:5]

#> 0.0394 0.0368 0.0343 0.032 0.0298

#> Z1 0 -0.01983922 -0.0390155 -0.05686517 -0.07358008

#> Z2 0 0.00000000 0.0000000 0.00000000 0.00000000

#> Z3 0 0.00000000 0.0000000 0.00000000 0.00000000

#> Z4 0 0.00000000 0.0000000 0.00000000 0.00000000

#> Z5 0 0.00000000 0.0000000 0.00000000 0.00000000The plot() function facilitates users in visualizing the

regularization path.

plot(fit, label = T)

It’s important to highlight that the prov.char parameter

here is also discretionary. In the absence of user input, the program

will automatically assign all observations to a single stratum by

default. Consequently, the conventional Cox model will be employed for

fitting.

fit.no_stratum <- Strat.cox(data, Event.char, Z.char, Time.char)

#> Warning: Provider information not provided. All data is assumed to originate

#> from a single provider!

coef(fit.no_stratum)[, 1:5]

#> 0.1745 0.1627 0.1517 0.1415 0.132

#> Z1 0 0.0000000 0.000000000 0.00000000 0.0000000000

#> Z2 0 0.0000000 0.000000000 0.00000000 0.0005808148

#> Z3 0 0.0155369 0.025755673 0.03313948 0.0398429622

#> Z4 0 0.0000000 0.004892787 0.01173321 0.0177767495

#> Z5 0 0.0000000 0.000000000 0.00000000 0.0000000000Likewise, the cv.strat_cox() function can be employed

for cross-validation, and the plot() function can be

utilized to visualize cross-validation error.

cv.fit <- cv.strat_cox(data, Event.char, Z.char, Time.char, prov.char, group = c(1, 2, 2, 3, 3), nfolds = 10, se = "quick")

cv.fit$lambda.min

#> [1] 0.004228925

plot(cv.fit)